Gujarat Board GSEB Textbook Solutions Class 12 Commerce Accounts Part 1 Chapter 7 Dissolution of Partnership Firm Textbook Exercise Questions and Answers.

Gujarat Board Textbook Solutions Class 12 Accounts Part 1 Chapter 7 Dissolution of Partnership Firm

GSEB Class 12 Accounts Dissolution of Partnership Firm Text Book Questions and Answers

Question 1.

Select the correct answer for each questions :

(1) How many methods are there for dissolution of a partnership firm ?

(A) One

(B) Three

(C) Two

(D) Four

Answer:

(C) Two

(2) Which of the following account is opened to incorporate the accounting effect of assets and liabilities of the partnership firm at the time of dissolution ?

(A) Profit and loss account

(B) Profit and loss appropriation account

(C) Revaluation account

(D) Realisation account

Answer:

(D) Realisation account

![]()

(3) What is the type of realisation account ?

(A) Balance sheet

(B) Personal

(C) Real

(D) Nominal

Answer:

(C) Real

(4) Which is the first payment made from the realisation of assets, at the time of the dissolution of a firm :

(A) Dissolution expense

(B) Loan of partner’s wife

(C) Liabilities towards third parties

(D) Partner’s loan

Answer:

(A) Dissolution expense

(5) Which of the following amount will be written at the credit side of realisation account, when there is balance of debtors ₹ 24,500 and bad debt reserve of ₹ 2,500 in the balance sheet at the time of the dissolution of a firm ?

(A) ₹ 24,500

(B) ₹ 2,500

(C) ₹ 22,500

(D) ₹ 27,000

Answer:

(B) ₹ 2,500

(6) To which account credit balance of general reserve, workmen accident compensation fund, – credit balance of profit and loss account is transferred at the time of the dissolution of a firm ?

(A) Realisation A/c

(B) Cash A/c

(C) Profit and loss A/c

(D) Partners’ capital A/c

Answer:

(D) Partners’ capital A/c

Question 2.

Answer the following questions in one sentence :

(1) Explain the meaning of dissolution of partnership.

Answer:

When business is not closed (shut) down due to retirement, death or insolvency of a partner or due to any other reasons and remaining partners keep business continuous, it is a dissolution of partnership.

![]()

(2) What is the dissolution of a partnership firm ?

Answer:

According to section-39 of Indian Partnership Act, when an partner get separated through dissolution of firm, that brings end of their partnership , it is known as dissolution of partnership firm.

(3) What is voluntary dissolution ?

Answer:

When all partners agree to dissolve the firm partnership firm can be dissolved at any point of time. It is called voluntary dissolution.

(4) Who has to bear dissolution expense, at the time of dissolution of a firm ?

Answer:

Generally dissolution expense of a firm has to borne by the firm itself, but in the most of the cases partner has to bear dissolution expense.

(5) How would you deal with the providend fund balance shown in the balance sheet at the time of dissolutions ?

Answer:

At the time of dissolution, the Providend Fund balance shown in the balance sheet will be transferred to credit side to Realisation Account.

(6) How would you deal with bad debts return, which is written off earlier ?

Answer:

At the time of dissolution, bad debts return which is written off earlier would be recorded on credit side of Realisation Account.

(7) Explain the meaning of Realisation Account.

Answer:

An account which is prepared at the time of dissolution to give the accounting treatments to dispose off assets and payments of liabilities is known as Realisation Account.

(8) Describe the methods of dissolution of a Partnership Firm.

Answer:

As per Indian Partnership Act- 1932, there are two methods for dissolution of partnership firm.

- Normal dissolution or dissolution without interference of court.

- Dissolution by the court.

![]()

(9) Where will you record the payment of bills payable under the second method of realisation account ?

Answer:

Under the second method of realisation account, payment of bills payable is credited to cash/ bank account and difference amount will be transferred to Realisation Account.

Question 3.

Answer the following questions in brief :

(1) Which accounts are prepared to close the books at the time of dissolution of a partnership firm ? Describe it.

Answer:

At the time of dissolution of firm, all assets of firm are sold and liabilities are paid from the realised income. If surplus remains, capital is redeemed and books of accounts are closed. On dissolution of firm, the following are the accounts are prepared to close the books of account:

(1) Realisation Account: All Asset accounts show debit balance and they are closed by credit in them and transferring the balances to the debit side of Realisation Account. Similarly, Liabilities have credit balances and they are debited to close them and are transferred to the credit side of Realisation Account.

(2) Partners’ Loan Account : If any partners have advanced a loan to the firm then his/her separate Loan Account is to be opened and closed by repaying the loan amount.

(3) Partners’ Capital/Current Accounts : After closing the Loan Account, the balance of the Current Account is transferred to the Partners’ Capital Account and then deficit is adjusted with Cash Account and Capital Account are closed.

(4) Cash/Bank Account : When Capital Account and Current Account are closed their balances are transferred to Cash Account and the total of Cash Account becomes equal from both side and firm’s account get automatically closed.

(2) In which circumstances court can pass the order for dissolution of a firm ? Explain

Answer:

When any partner file a suit for dissolution of a firm on any of the following circumstances and the court orders to dissolve the firm :

- When any partner become insolvent.

- When any partner becomes of unsound mind.

- When a partner willfully and persistently breaches the partnership agreement.

- When a partner undertakes misconduct against partnership firm or against business of firm.

- When a partner becomes permanently incapable of performing his duties as a partner.

- When a firm continuously incurs losses and is unable to run a business due to loss.

- When a partner transfers his whole interest in the partnership to a third party without the consent of other partners.

- When the court finds any other ground to be just and equitable for the dissolution of the firm.

(3) Write short note : Realisation Account.

Answer:

The account which is prepared to incorporate accounting treatments for disposal or liabilities and assets of the firm is known as Realisation Account.

- On the debit side of this account, the balance of all assets are transferred and on the credit side all liabilities are transferred.

- The liabilities which are paid off one by one are recorded on debit side of Realisation Account. If account shows credit balance then it is treated profit and credited in partners capital account in their profit and loss sharing ratio.

- The differences of realisation account will be either profit or loss. This different is allocated between the partners in their profit sharing ratio. Profit is credited to their capital account and loss is debited to their capital account.

![]()

(4) How would you deal with the following balances disclosed in the balance sheet at the time of the dissolution of a partnership firm ? Explain.

(i) General Reserve

(ii) Investment Fluctuation Fund

(iii) Workmen Accident Compensation Fund

(iv) Providend Fund

(v) Debit Balance of Profit and Loss A/c

(vi) Depreciation Fund

Answer:

(i) General Reserve : Balance of general reserve account is credited to partners’ capital or current account in their profit and loss sharing ratio.

(ii) Investment Fluctuation Fund : Investment Fluctuation Fund is a provision against assets which will be shown under the heading of provision on credit side of Realisation Account.

(iii) Workmen Accident Compensation Fund : Workmen Accident Compensation Fund is a accumulated profit, which will be credited for all partners’ capital/current account in their profit-loss sharing ratio.

(iv) Providend Fund : Providend Fund is a liability (debt) which will be shown under the heading of Sundry Liability on credit side of Realisation account.

(v) Debit Balance of Profit and Loss A/c : Debit balance of profit and loss account will be debited to partners’ capital account in their profit and loss sharing ratio.

(vi)

Depreciation Fund : Depreciation Fund is a provision against asset which will be shown under the heading of provision on credit side of Realisation Account.

(5) Describe the legal provisions pertaining to loss of dissolution of a partnership firm.

Answer:

According to Indian Partnership Act, the loss arised including capital deficit at the time of dissolution is executed in the following manner:

(a) First of all it will be written off from the profit of the firm.

(b) If profit is not sufficient, then it will be paid from the capital of the partners.

(c) If capital is not sufficient, then all partners would distribute this loss in their profit-loss sharing ratio and pay from their personal assets as per requirement.

(6) Explain the normal procedure of partnership firm dissolution.

Answer:

Normal Procedure of Dissolution : (i) First of all any expenses pertaining to dissolution of the firm are paid, (ii) Then after liabilities towards third parties are paid. Loan of partner’s wife will be treated as a liability of toward the third party, (iii) Then after from the remaining amount loan given by the partners are paid, (iv) And at last capital and current accounts balances of partners are paid, (v) Beside this, if any amount remains, then that amount is distributed between partners in their profit and loss sharing ratio.

![]()

Question 4.

Answer the following questions to the point:

(1) Distinguish between : First and Second method of disposal of realisation account.

Answer:

Difference between first and second method of disposal of realisation account is as under:

| Points | First Method | Second Method |

| 1. Realisation Account | After closing the assets and liabilities accounts, they are transferred to Realisation account. | In Realisation Account, assets and liabilities accounts are not transferred. |

| 2. Accounts | Liabilities and Assets accounts | Accounts of Liabilities and are closed. Assets are not closed. |

| 3. Realisation of Assets | On credit side of Realisation Account, the realised value on sale of asset are recorded. | Realised value of the assets is credited to assets account and the balance is transferred to Realisation Account. |

| 4. Payment of Liability | On debit side of Realisation Account payment for the liability is shown. | If liability is debited to that liability A/c. the amount paid towards it is transferred to Realisation Account. |

| 5. Circumstances | If the liabilities are paid immediately and the assets are realised immediately on dissolution, then this method is suitable. | If the payment of liability and the realisation of assets are made in instalments on disso lution, then this method is suitable. |

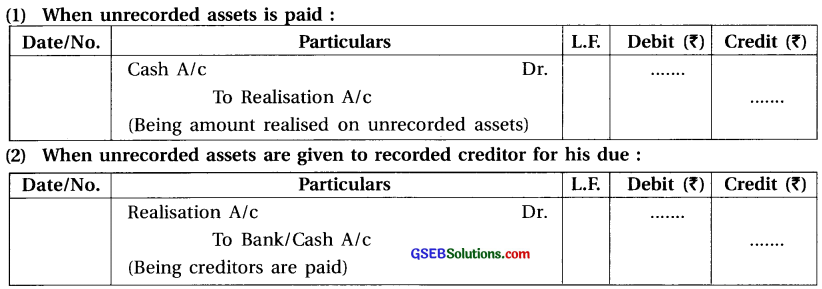

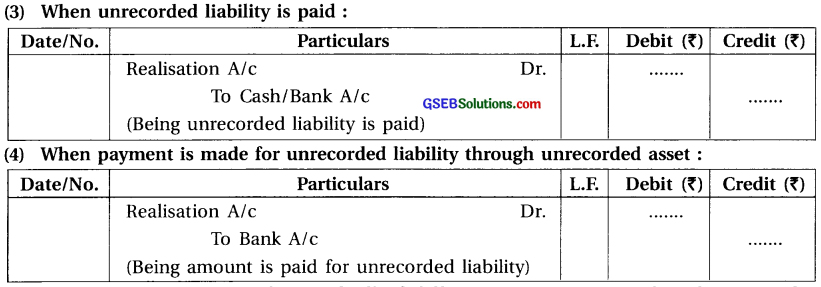

(2) How would you undertake accounting disposal of realisation of asset and payment of liability which are not recorded in the balance sheet at the time of the dissolution of a firm ? Explain.

Answer:

Accounting disposal of realisation of assets and payment of liability which are not recorded in the balance sheet at the time of dissolution of a firm is as under :

(3) Give accounting treatments for goodwill of different circumstances when firm goes for dissolution.

Answer:

Following are the accounting treatments for goodwill of different circumstances when firm goes for dissolution :

(1) If the value of goodwill will be shown in the balance sheet then like other assets, goodwill will be shown as debit side of Realisation Account. (2) Amount realised from the sale of goodwill will be shown on credit side of Realisation Account. (3) If no information regarding realisation of goodwill is given then it is to be understood that nothing is realised. (4) At the time of dissolution of firm, if goodwill is not shown in the books of account, hence amount realised • then it will be treated as profit and credited to Realisation Account. (5) When any partner purchase whole business (including goodwill) then (i) Capital account of business purchase partner is debited by amount of goodwill and (ii) Realisation account is credited by amount of goodwill.

![]()

(4) Explain in brief, legal provisions of accounting settlement for partnership firm dissolution.

Answer:

The main legal provisions with regards to dissolution a of partnership firms are as follows :

(1) Legal provision for loss of firm : Here, from the profits of the firm and if profits is not . sufficient the loss of the firm is written off against the capital of the partners. If capitals are insufficient, the loss will be borne by the partners in their profit and loss ratio and will be paid by selling of their own assets.

(2) Legal provision for the payment of liabilities of the firm and partners : The partners have unlimited liabilities and liabilities of the firm are to be paid off by assets of the firm but because of unlimited liabilities of the partners, firm’s remaining liabilities are to be paid of from their personal assets.

(3) Payment of loan to the firm by the partners : First of all liabilities of the firm will be paid ‘ by realising the asses of the firm. After paying the external liabilities of the firm, loan of

partner’s will be paid. If more than one partner has loaned to the firm and if the partners are not in a position to make up deficit, the loans are to be paid proportionately.

(4) Payment of loan given by the partners’ wife : Wife’s loan to the firm will be rapid like payment to a third party. But if wife of a partner has given it from the fund of her husband, it will be treated as loan of that partner.

(5) Payment of liabilities of a partner : Liabilities of the partners are unlimited and if any of partners is declared insolvent on dissolution, the solvent partners are liable to pay the liabilities of the firm as the insolvent partner/s will not be able to meet his/their share.

(6) Legal provision for distribution of the realised assets of the firm : The payment for the liability from the realisation of assets will be made in following manner.

(i) First pay the dissolution expenses.

(ii) After that, liabilities of third parties will be paid.

(iii) Then, the loan of partner/s is to be paid.

(iv) Payment towards partners capital and current accounts.

(v) If any surplus, it will be distributed among the partners in the profit-loss sharing ratio.

(5) Explain methods of dissolution without the interference of court.

Answer:

There are two method for dissolution of partnership firm : (I) Normal Dissolution (II) Dissolution by the court.

(I) Normal Dissolution/Dissolution without interference of Court : It is as under :

(i) By agreement: When all partners agree to dissolve the firm, partnership firm can be dissolved at any point of time. It is voluntary dissolution.

(ii) Dissolution on happenings of certain contingencies :

(a) If arrangement for a fixed term, by the expiry of that term.

(b) If arrangement to carry out specific aim, by the completion thereof.

(iii) Dissolution by notice : Where the partnership is at will, the firm may be dissolved by any partner giving notice in writing to all the other partners of his intention to dissolve the firm.

(iv) Dissolution as per act : In the following conditions compulsory dissolution is taken place by the act.

(a) When all the partners of the firm become insolvent, or except one, all partners become insolvent.

(b) When business of firm becomes illegal, this also brings dissolution of a partnership firm. E.g. If a firm doing business of Tobacco and government put restriction through law on this business, then this business automatically become illegal and dissolve.

(c) When any partner becomes mental weak or due to his death. Partnership is going to end and firm dissolve.

(v) Dissolution as per contract: Dissolution of a partnership firm can be done on the basis of predetermined contract between the partners.

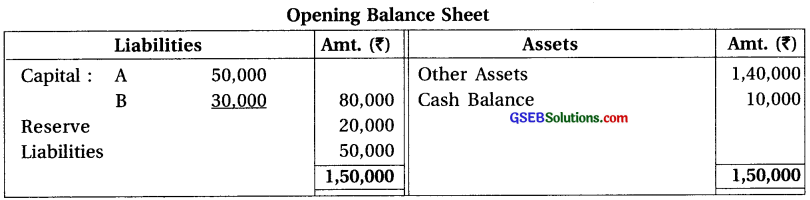

(6) Total assets are ₹ 1,50,000 of firm A and B where cash of ₹ 10,000 is included. Net assts of the firm are ₹ 1,00,000. The ratio of capital and reserve is 4 : 1. The capital of A is more than of B by ₹ 20,000. Loss of realisation account is ₹ 20,000. Firm is dissolved. Prepare opening balance sheet and ascertain opening capital of A and B.

Answer:

Note:

(1) Other Assets = Total Assets – Cash

= ₹ 1,50,000 – ₹ 10,000

= ₹ 1,40,000

(2) Net Assets = Total Assets – Total Liabilities

∴ ₹ 1,00,000 = ₹ 1,50,000 – Total Liabilities

∴ Total Liabilities = ₹ 1,50,000 – ₹ 1,00,000

= ₹ 50,000

(3) Capital + Reserve + Liabilities = Total Assets

∴ Capital + Reserve + ₹ 50,000 = ₹ 1,50,000

∴ Capital + Reserve = ₹ 1, 50,000 – ₹ 50,000

(4) Ratio of Capital and Reserve = 4 : 1

∴ Capital = ₹ 1,00,000 × \(\frac {4}{5}\) = ₹ 80,000

∴ Reserve = ₹ 1,00,000 × \(\frac {1}{5}\) = ₹ 20,000

(5) Here, capital of A is more than of B by ₹ 20,000

Suppose capital of B is x. Capital of A = x + ₹ 20,000

∴ Total Capital = x + x + ₹ 20,000 = ₹ 80,000

∴ 2x = ₹ 80,000 – ₹ 20,000

∴ 2x = ₹ 60,000 ∴ x = ₹ 30,000 ∴ Capital of B = ₹ 30,000

Now, Capital of A = x + First Flight 20,000 = ₹ 30,000 + ₹ 20,000 = First Flight 50,000

![]()

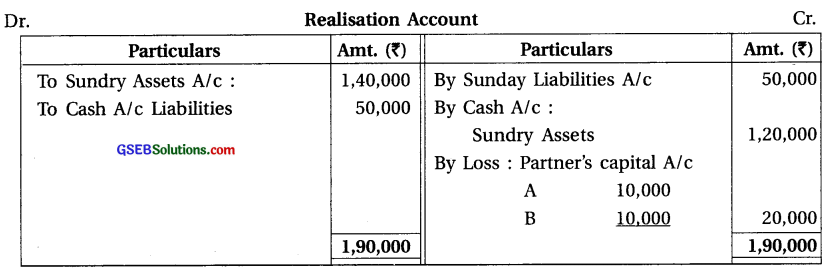

(7) Prepare realisation account from Question No. 6.

Answer:

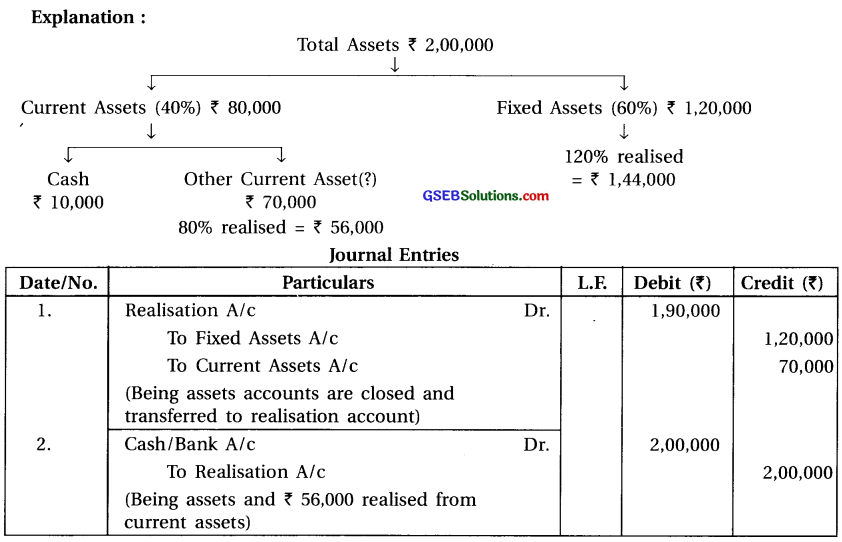

(8) Total Assets of firm at the time of dissolution is ₹ 2,00,000. Out of which 40% are current assets (including cash f 10,000). 120% realised for fixed assets. While 80% are realised of current asset. Pass journal entries.

Answer:

Question 5.

Pass journal entries for the following of firm in the case of firm’s dissolution :

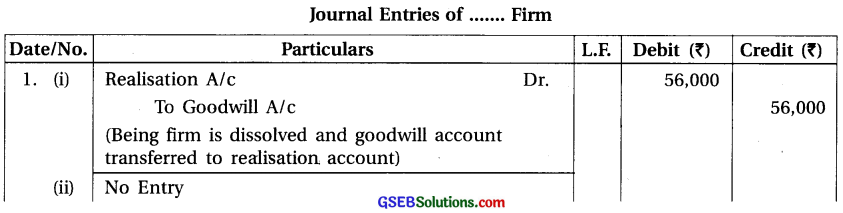

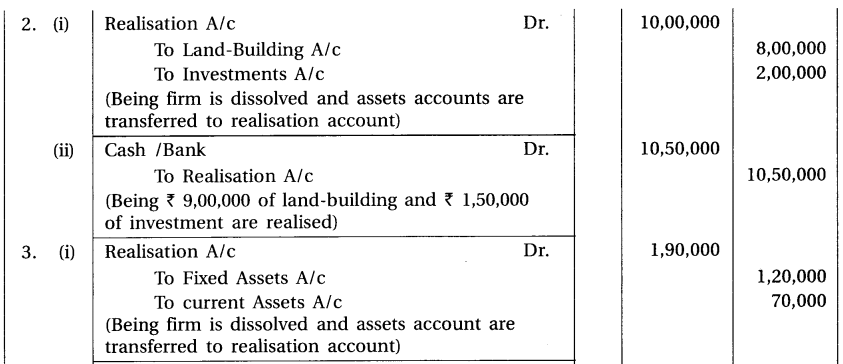

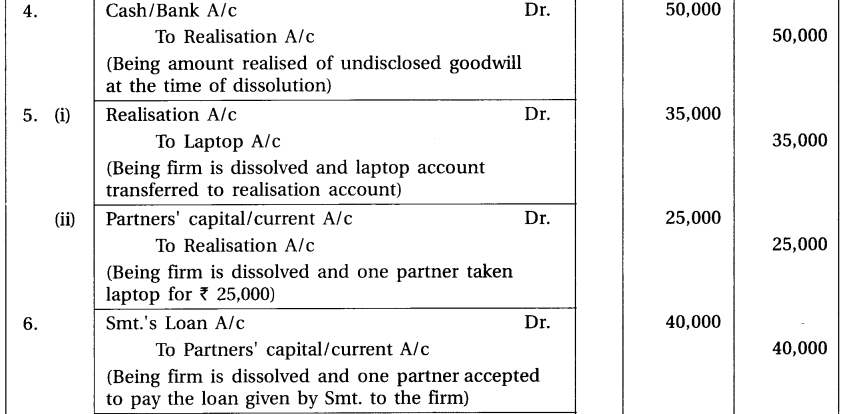

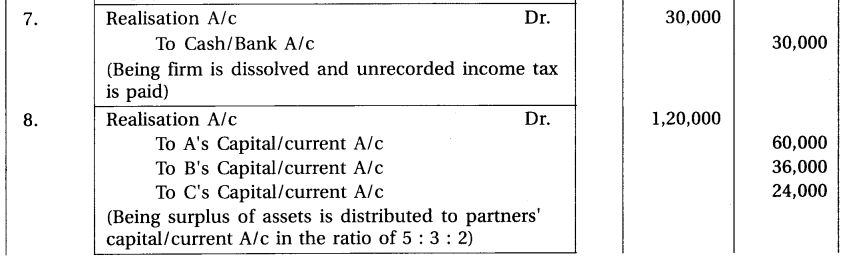

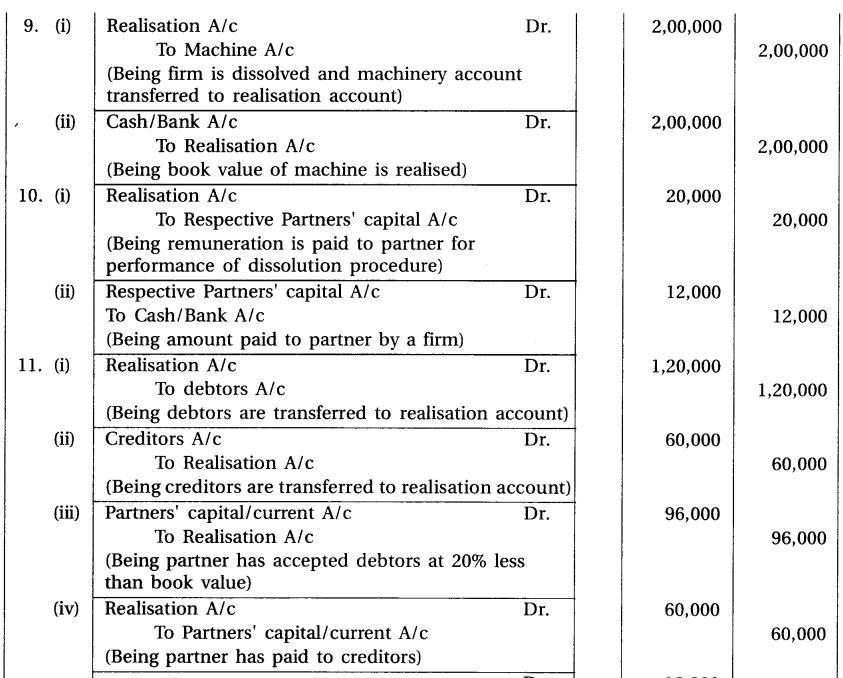

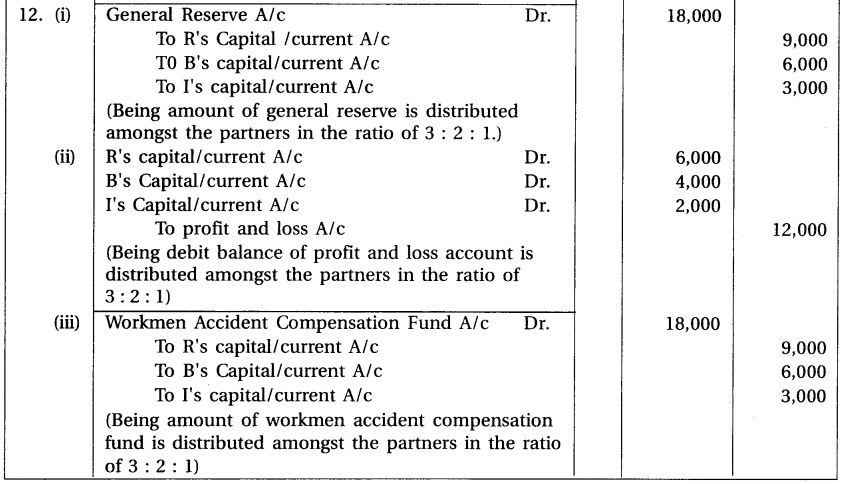

(1) At the time of dissolution the book value of goodwill is ₹ 56,000. No amount is realised. (2) In the balance sheet land-building ₹ 8,00,000 and investments of ₹ 2,00,000 are disclosed. Respectively ₹ 9,00,000 and ₹ 1,50,000 are realised from them. (3) Total assets of the firm are ₹ 2,00,000 out of which 40% of are current assets (including cash of ₹ 10,000). Book value is realised. (4) Goodwill is not disclosed in the book. But ₹ 50,000 are realised during dissolution. (5) The value of laptop is ₹ 35,000. One partner has taken it for ₹ 25,000. (6) A partner has accepted to pay loan of his Smt. ₹ 40,000, which was given to the firm. (7) Income tax liability is now payable ₹ 30,000 it is not recorded in the book. (8) After making payment of all liabilities and loan of partners of firm, surplus of assets is ? 1,20,000. The profit and loss sharing ratio of partners A, B and C are 5 : 3 : 2. (9) Machine is disclosed in the book at the time of dissolution for ₹ 2,00,000. Book value is realised. (10) One partner has accepted responsibility to undertake dissolution procedure. In the return of it, decided to pay remuneration of ₹ 20,000. On account of expense firm has paid him ₹ 12,000. (11) There are debtors of ₹ 1,20,000 and creditors of ? 60,000 at the time of dissolution of firm. One partner has taken debtors at 20% than book value less and accepted to pay creditors. (12) The profit-loss sharing ratio between partners R, B and I is 3 : 2 : 1. Undertake the disposal of the following balances : (i) General reserve ₹ 18,000 (ii) Debit balance of profit and loss A/c ₹ 12,000 (iii) Workmen accident compensation fund ₹ 18,000.

Answer:

![]()

Question 6.

Pass journal entries for the following transactions, when realisation account is prepared:

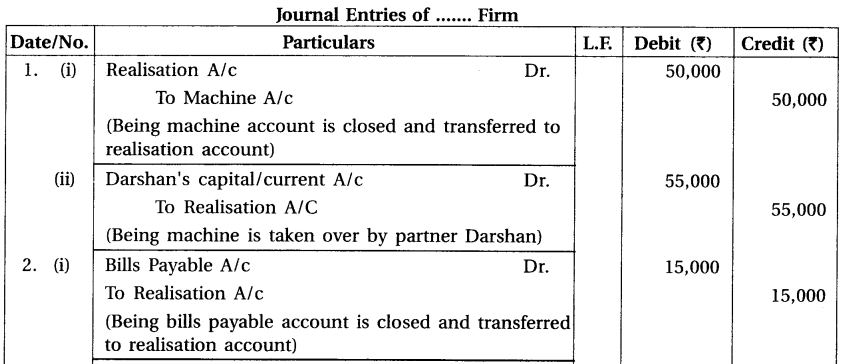

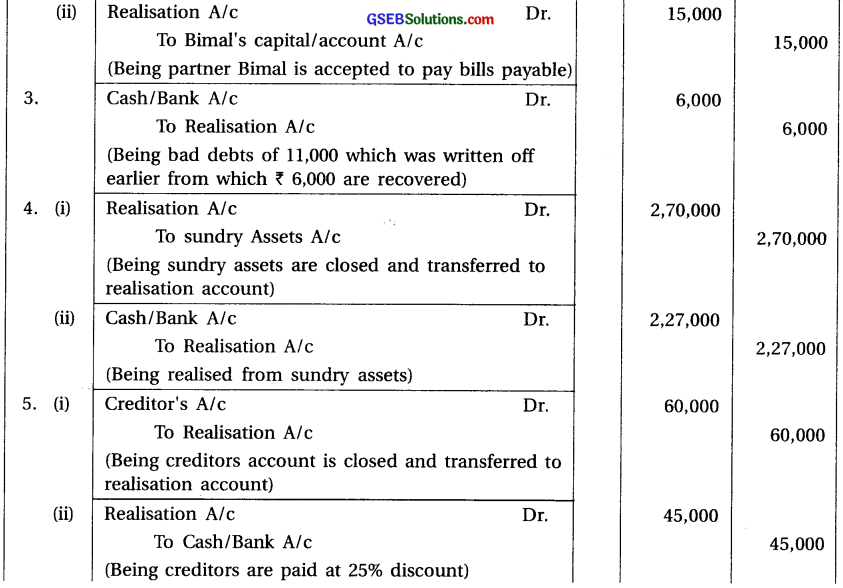

(1) Book value of machine is ₹ 50,000, which is taken over by partner Darshan for ₹ 55,000. (2)

Partner Bimal has accepted to pay bills payable of 15,000. (3) Past bad debts was written off

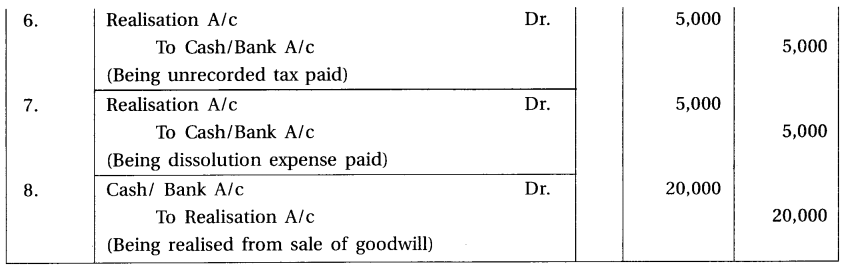

11,000 out of which 6,000 are recovered. (4) Book value of sundry assets is ₹ 2,70,000 and realised ₹ 2,27,000. (5) Sundry creditors ₹ 60,000, paId at 25% discount. (6) Unrecorded tax paid ₹ 5,000. (7) Dissolution expense paid ₹ 5,000. (8) Goodwill Is not disclosed in the books. But ₹ 20,000 realised from sale of it, at the time of dissolution.

Answer:

Question 7.

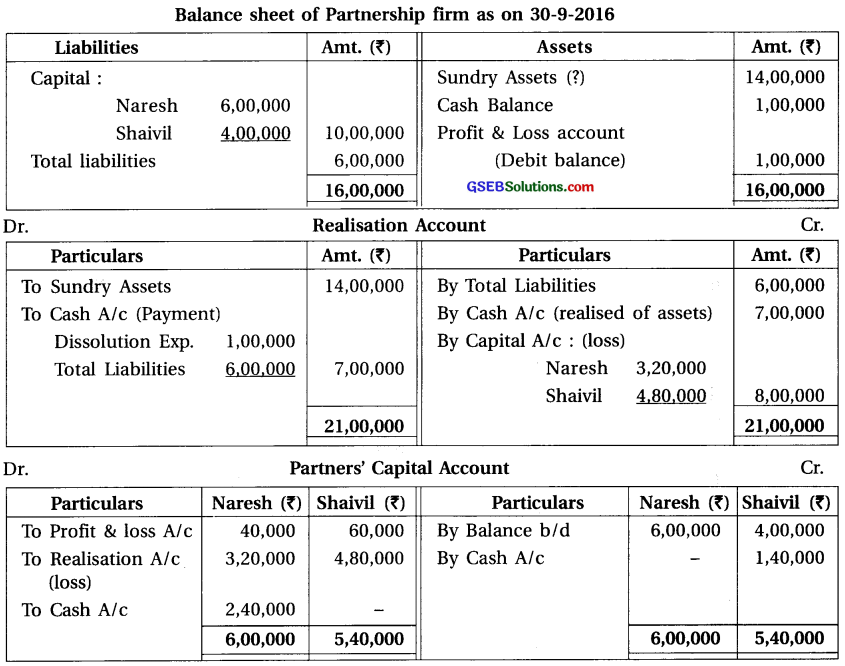

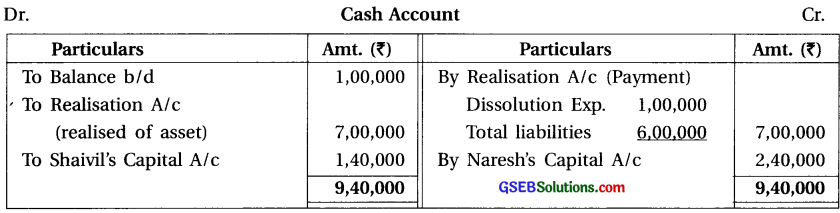

Naresh and Shaivil are partners sharing profit-loss in the proportion of 2 : 3. On 30-9-2016. They have decided to dissolve the firm. On this date their capital was ₹ 6,00,000 and ₹ 4,00,000 respec-tively. Total liabilities of the firm are ₹ 6,00,000. The balance of accumulated debit balance of profit and loss account is ₹ 1,00,000 and cash balance is ₹ 1,00,000, 50% are realised from assets of firm. Dissolution expense is ? 1,00,000.

Prepare necessary accounts to close books of the firm.

Answer:

Here, balance sheet before dissolution is not given. So, first of all prepare balance sheet and then prepare the accounts of dissolution.

Note :

(i) By preparing opening balance sheet of partnership firm, difference amount of assets side ₹ 1,40,000 will be considered as sundry assets, (ii) There is no information, so whole amount of liability will be paid, (iii) 50% means ₹ 70,000 of sundry assets of the firm are realised.

![]()

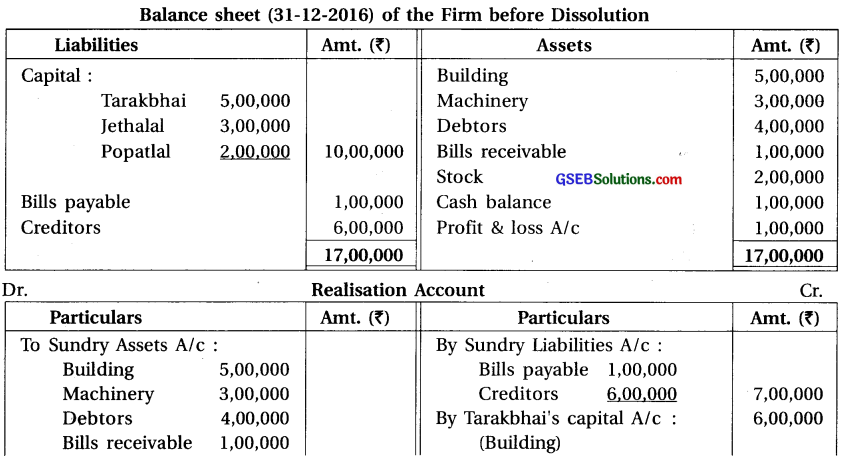

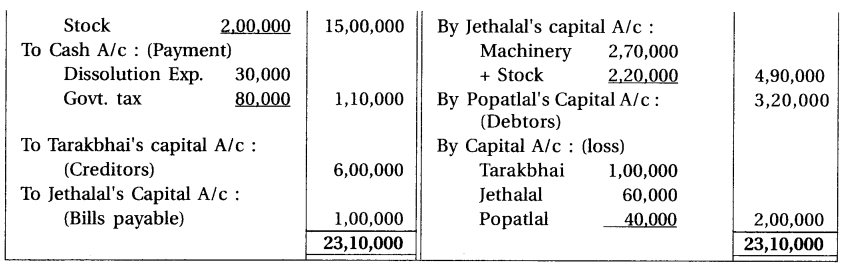

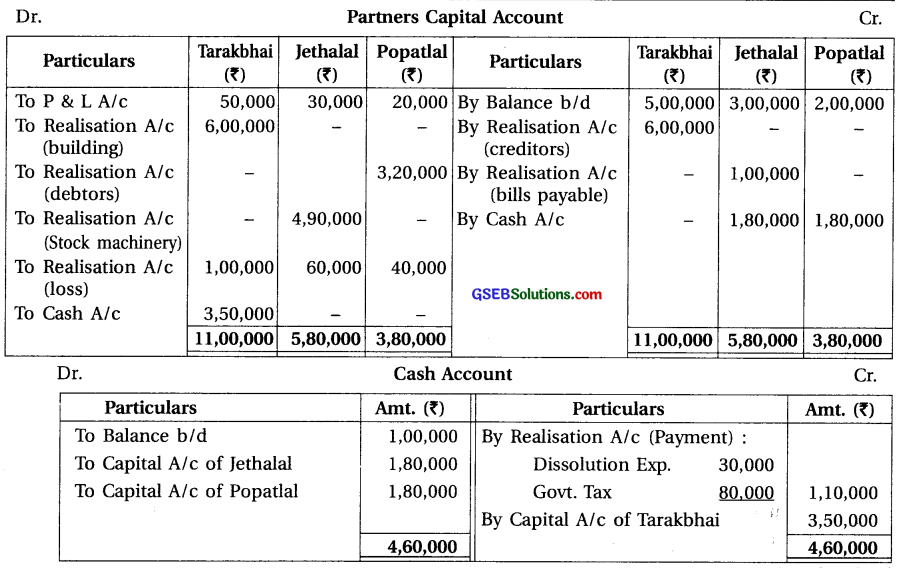

Question 8.

On 1-1-2015, Tarakbhai, Jethalal and Popatlal are commenced partnership firm to share profit- loss in the proportion of 5 : 3: 2. Their capital on that date was ₹ 5,00,000, ₹ 3,00,000 and ₹ 2,00,000. On 31-12-2016, they have decided to dissolve the firm. On this date the status of the firm was as follows :

Building ₹ 5,00,000

Debtors ₹ 4,00,000

Stock ₹ 2,00,000

Machinery ₹ 3,00,000

Bills receivable ₹ 1,00,000

Creditors ₹ 6,00,000

Bills payable ₹ 1,00,000

Cash balance ₹ 1,00,000

Debit balance of profit and loss A/c ₹ 1,00,000

Since firm was loss making, it is dissolved and the disposal of assets and liabilities are as follows :

(1) Tarakbhai has taken over building at 20% more than book value against which accepted to pay to the creditors. (2) Jethalal has taken machines at 10% less and stock at 10% more than book value. He has accepted to pay bills payable. (3) Poptalal has taken debtors at 20% less than book value.

Note : (1) Bills receivable becomes valueless. (2) Outstanding government tax paid X 80,000. (3) Dissolution expense of firm X 30,000.

Your are asked to prepare realisation account, partners capital accounts and cash account.

Answer:

![]()

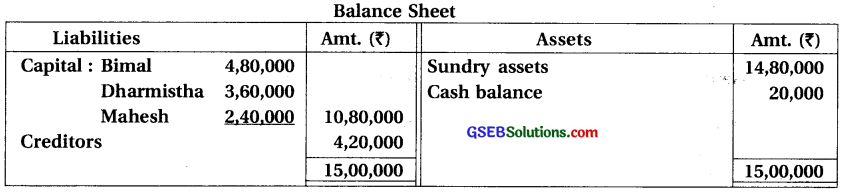

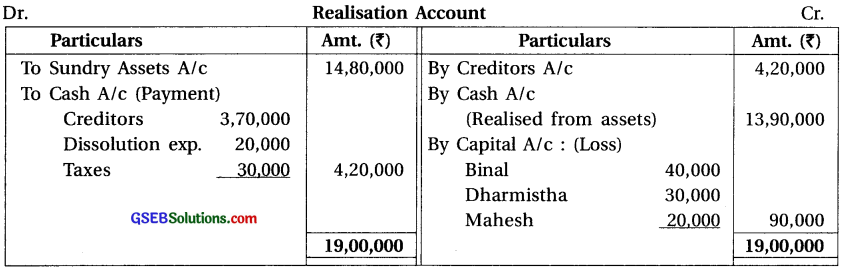

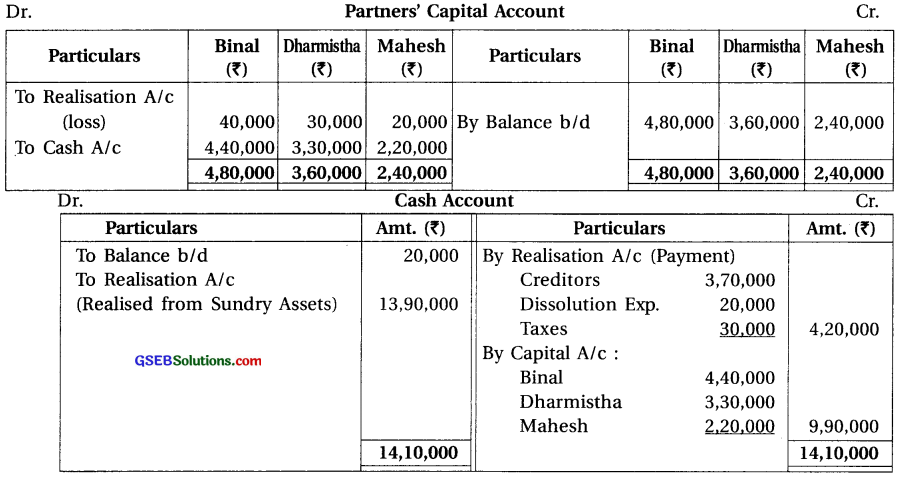

Question 9.

Binal, Dharmistha and Mahesh are partners sharing profit-loss in the ratio of 4 : 3 : 2. Firm dissolved on 30-9-2016. On that day the status of the firm was as follows :

(1) ₹ 13,90,000 realised from sundry assets. (2) Creditors are paid ₹ 3,70,000 as a final settlement. (3) Dissolution expense paid ₹ 20,000. (4) ₹ 30,000 paid for unrecorded taxes. (5) Prepare necessary accounts.

Answer:

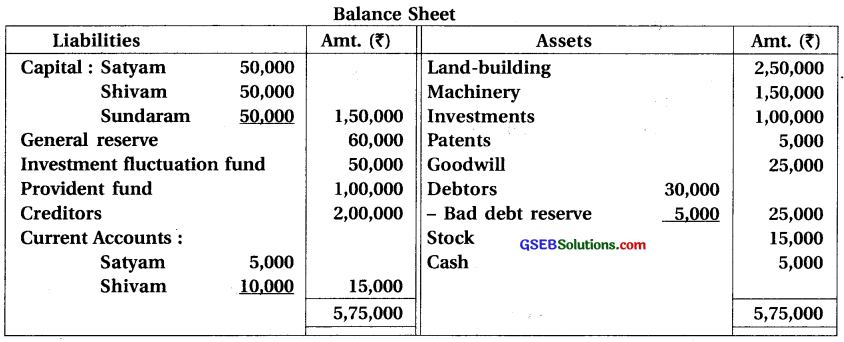

Question 10.

Satyam,Shivam and Sundaram are partners sharing profit-loss in the proportion of \(\frac {1}{2}\) : \(\frac {1}{3}\) : \(\frac {1}{6}\). The balance sheet of their firm as on 31-12-2016 is as under :

The firm was dissolved on 1st January, 2017. Disposal of assets and liabilities was done as under:

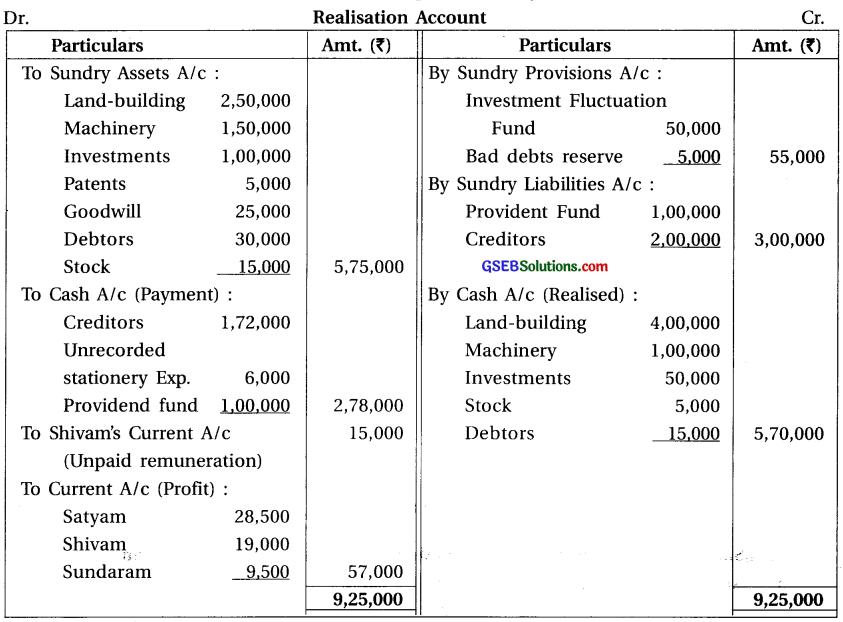

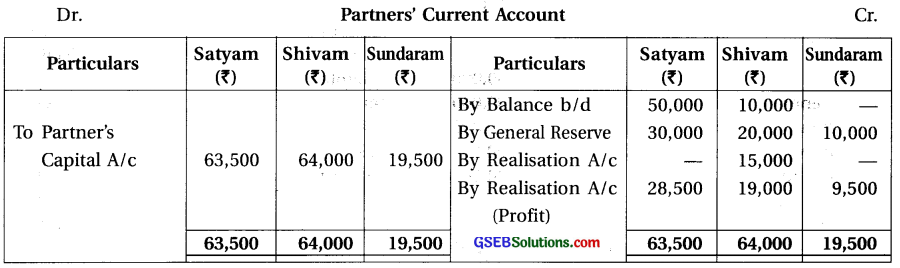

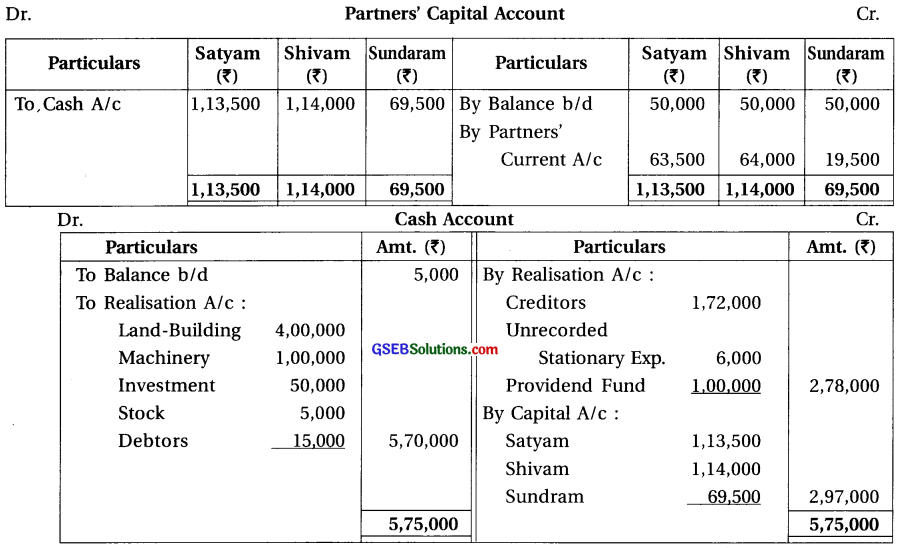

(1) Sale of land and building ₹ 4,00,000, machinery ₹ 1,00,000, investments ₹ 50,000 and stock ₹ 5,000. (2) From debtors ₹ 15,000 are received write off remaining. (3) Out of total creditors, a creditor of 10% was given unrecorded investments of ₹ 10,000 and remaining amount paid in cash. Remaining creditors are paid at 10% discount. (4) Unrecorded expense of stationery ₹ 6,000 paid to Arihant Stationery Mart. No amount is realised for goodwill and patent. (5) A remuneration of ₹ 15,000 was decided to pay to Shivam to perform dissolution procedure. Actual dissolution expense ₹ 6,000 paid by Shivam. (6) Prepare necessary accounts to close books of the firm.

Answer: